Prospect Theory - Psychology

Imagine you're offered a choice between two options:

An equal chance to have either $1 million or $9 million

A guaranteed $5 million

Which would you choose? Most people opt for the certainty, even though the expected value of both choices is the same ($5 million). This preference for certainty over risk, even when the expected outcomes are equal, is a fundamental aspect of human decision-making.

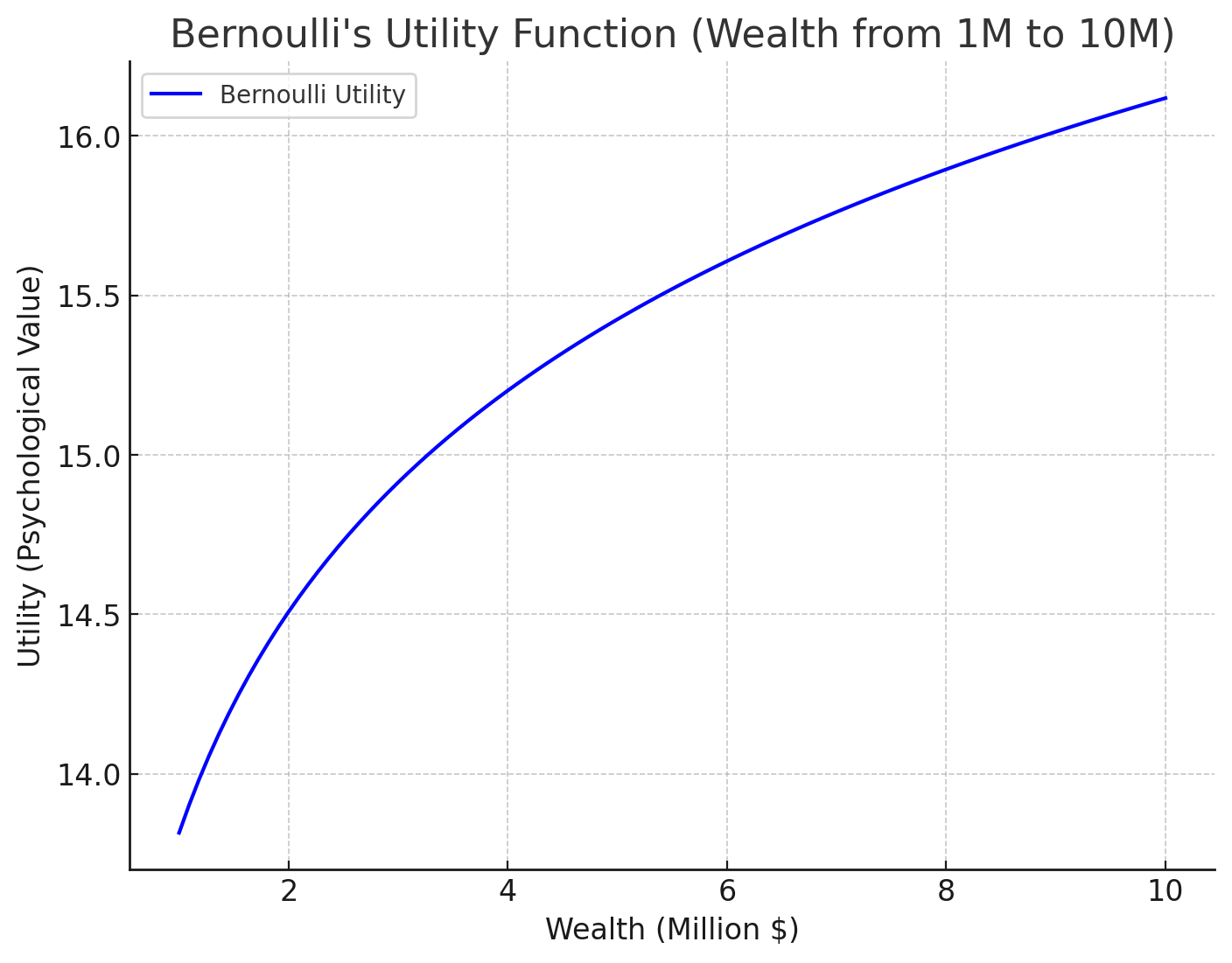

Bernoulli's Utility Theory

In the 18th century, Daniel Bernoulli proposed a groundbreaking idea to explain risk aversion. He introduced the concept of "utility" – the psychological value people assign to different outcomes. Bernoulli's utility function can be expressed as:

U(w) = ln(w), where w is wealth

This logarithmic function creates a concave curve, showing that the utility of wealth increases at a decreasing rate. In our initial example, despite the equal expected monetary value, the expected utility of the risky choice (0.5 * ln(1) + 0.5 * ln(9) ≈ 1.08) is lower than the utility of the certain choice (ln(5) ≈ 1.609). This mathematical framework helps explain why people tend to prefer certainty.

But the utility theory had a crucial flaw: it assumed people evaluate outcomes based on total wealth rather than changes in wealth. In reality, people tend to assess situations relative to their current circumstances.

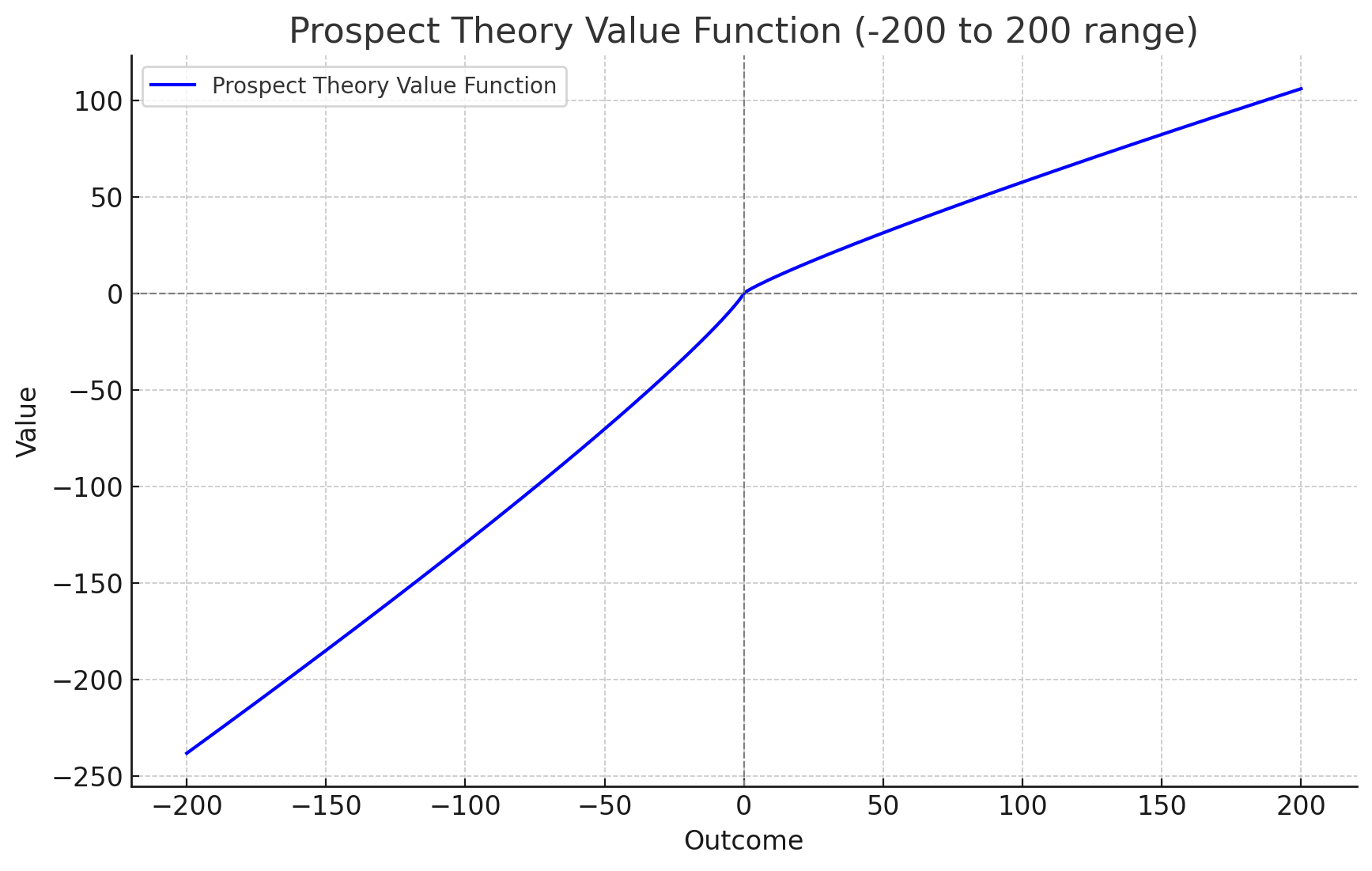

Prospect Theory

Developed by Daniel Kahneman and Amos Tversky in 1979, prospect theory aims to address the shortcomings of the utility theory and better model how people make decisions under uncertainty. The theory incorporates three key principles:

Reference Point: People evaluate outcomes relative to a reference point, often their current wealth, rather than in absolute terms.

Loss Aversion: Losses have a greater psychological impact than equivalent gains. People are more sensitive to losing $100 than to gaining $100.

Diminishing Sensitivity: Similar to utility theory, the impact of both gains and losses diminishes with size.

The prospect theory value function can be visualised as an asymmetrical S-shaped curve, steeper for losses than for gains.

where x is the change in wealth relative to a reference point; α, β ∈(0,1) are risk aversion parameters; λ is the loss aversion parameter.

To illustrate the importance of the reference point, let's revisit our initial scenario with two individuals, A and B:

A's current wealth is $1 million

B's current wealth is $9 million

Given the same choices:

Equal chance of $1 million or $9 million

Guaranteed $5 million

A and B are likely to make different decisions:

For A, the first option presents a 50 / 50 chance—either no change or a significant gain. Meanwhile, the second option guarantees a 400% increase ($4 million), making it clearly more appealing.

For B, however, the second option means a guaranteed 44% loss ($4 million). In contrast, the first option offers either no loss or a potential loss, each with equal probability. Given this, B is more inclined to take the gamble rather than accept a definite loss.

These differing perspectives, shaped by their current wealth (reference point), will likely lead A and B to make different choices despite facing the same options.

Conclusion

Prospect theory introduces “relativity” into our understanding of decision-making under uncertainty. It provides a more accurate model of human behaviour than the traditional utility theory.